Where the Money Goes in Pet (And Who Controls It)

Pet industry investors aren't a monolith. VCs, PE firms, corporate strategics, and angels each operate on different timelines with different return expectations. This is the map to who actually funds pet companies and how deals get done.

Blackstone paid $2.3 billion for Rover in November 2023. A pet-sitting marketplace. The same month, a pet food startup with real revenue and real margins couldn't close a $5 million Series A. Same industry, opposite outcomes. The difference wasn't the business. It was the investor.

Pet industry investors aren't a monolith. The VC writing a $500K seed check into a veterinary tech startup operates on different incentives than the PE firm rolling up dog daycares at 8x EBITDA. The corporate strategic acquiring a diagnostics company wants something neither of them want. Founders who treat "raising capital" as a single problem end up pitching the wrong investors with the wrong story at the wrong stage.

This is the map to who actually funds pet companies, what they're looking for, and how sophisticated founders navigate the landscape.

Why Pet Attracts Capital Right Now

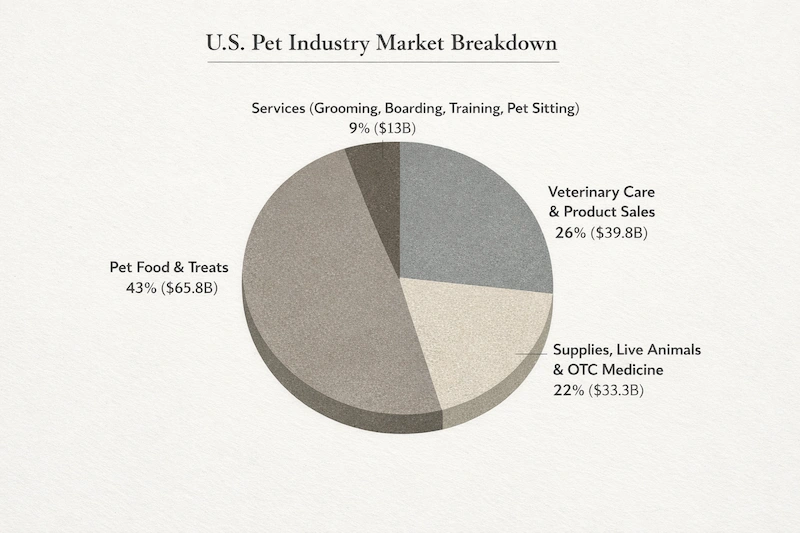

Pet industry investment follows a simple thesis: Americans spent $147 billion on their pets in 2023, and that number keeps climbing. The pet tech segment alone hit $14.6 billion in 2025 and is projected to reach $61.7 billion by 2035. Investors see a massive, growing market with emotional buying behavior and proven willingness to pay premium prices.

The capital flow reflects this. Pet companies raised $2.4 billion globally between 2023 and 2025. The first half of 2025 saw $192 million deployed across 17 rounds, a 68.85% increase year-over-year. Venture capital targeting AI-driven pet health startups has increased significantly, with some estimates suggesting 45% growth over the same period.

The "recession-resistant" narrative helps. Pet spending held up during both the 2008 financial crisis and the 2020 pandemic. Investors who got burned in discretionary consumer categories see pet as a safer bet. Whether that thesis holds through a prolonged downturn remains untested at current market sizes.

The Four Types of Pet Investors (And What Each Actually Wants)

Pet industry investors segment into four distinct categories. Each operates on different timelines, with different return expectations, and different definitions of success. Pitching a PE firm the way you'd pitch a seed-stage VC is a waste of everyone's time.

Venture Capital: Growth at All Costs (Sometimes)

Generalist VCs entered pet aggressively between 2019 and 2022. Sequoia backed Rover and PetPlate. Andreessen Horowitz invested in BarkBox and NomNomNow. Greycroft built a portfolio including The Farmer's Dog and Wag. These firms write checks from $1 million to $50 million depending on stage, and they optimize for hypergrowth that leads to billion-dollar outcomes.

The catch: generalist VCs have largely cooled on pet after the D2C bloodbath. The firms that remain active want recurring revenue, defensible technology, or clear paths to market leadership. One-time purchase businesses, hardware without software margins, and "better pet food" pitches struggle to get meetings.

Dedicated pet-focused funds have emerged to fill the gap. Ani VC positions itself as the first independent early-stage venture fund for the pet industry, with advisors including Anna Skaya, former CEO of Basepaws (acquired by Zoetis in 2022). Pawsible Ventures launched a $10 million Fund I in October 2024, writing $100K to $500K checks into 15-20 early-stage pet health and wellness startups over three years. TAW Ventures, founded by Jane Lauder in January 2025, focuses on pet wellness, health, and longevity, partnering with Leap Venture Studio to support their accelerator cohorts.

These dedicated funds offer something generalist VCs can't: industry-specific expertise, relevant networks, and thesis alignment that doesn't require convincing a partner that pet is a real category.

Private Equity: Cash Flow and Consolidation

Private equity approaches pet differently. Where VCs seek growth, PE seeks cash flow. Where VCs want to build category leaders, PE wants to roll up fragmented markets.

Frontenac operates one of the most visible PE strategies in pet through its platform company Digs Dog Care. The firm targets middle-market operators with $5-40 million in EBITDA, writing $50-150 million equity checks. Digs is on track to close 15 add-on acquisitions in 2025 alone, buying dog daycares, boarding facilities, and grooming businesses to build regional density.

Blackstone's Rover acquisition represents the other end of the PE spectrum: a $2.3 billion bet on a scaled platform with network effects. That deal signaled to the market that pet services businesses could command tech-company multiples if they achieved sufficient scale and recurring revenue characteristics.

The pattern is clear. PE wants businesses that generate predictable cash, operate in fragmented markets ripe for consolidation, and don't require continuous reinvention. If your business needs to spend heavily on R&D or customer acquisition to stay competitive, PE isn't your buyer.

Corporate Strategic: Capability Acquisition

Mars Petcare, Nestle Purina, Zoetis, and a handful of other giants treat acquisitions as capability purchases. They're not buying revenue. They're buying technology, talent, or market position they can't build internally.

Zoetis acquiring Basepaws in 2022 illustrates the model. Basepaws had built a consumer-facing genetic testing business for cats, but Zoetis wanted the underlying technology and data for its veterinary diagnostics pipeline. The consumer brand was incidental.

Corporate strategics pay premium prices when the capability gap is wide and time-to-market matters. They pay less for businesses that compete directly with their existing operations. And they move slowly. The founder who thinks they're six months from a strategic exit is usually eighteen months away, minimum.

Angels and Syndicates: The Industry Network

The pet industry's angel investor ecosystem is smaller and more networked than most founders expect. Many active angels are former operators who sold their own pet businesses and now deploy capital into the next generation.

PetCareVC structures syndicated investments through AngelList, pooling capital from pet industry founders, operators, and investors to write smaller checks that make deals accessible to a broader community. These syndicate members often provide something more valuable than capital: introductions to retailers, manufacturers, and later-stage investors.

Industry-specific angels evaluate opportunities differently than financial angels. They pattern-match against their own operational experience, which can be a blessing (useful advice, warm introductions) or a curse (reflexive skepticism toward business models that didn't exist when they were operating). Founders raising from industry angels should expect detailed operational questions that generalist investors wouldn't think to ask.

What's Getting Funded (And What's Getting Passed)

Capital doesn't flow evenly across pet categories. The sectors attracting investment share common characteristics. The sectors struggling to raise share different ones.

Hot: Veterinary Technology

Modern Animal raised $46 million in Series D funding for its veterinary care model. Airvet closed an $11 million Series B-2 for telehealth. Investors see veterinary care as the highest-value transaction in the pet ecosystem, and technology that improves access, reduces costs, or enhances outcomes commands attention.

The veterinary labor shortage adds urgency. The industry faces a structural deficit of veterinarians and technicians that won't resolve through traditional hiring. Technology that extends the capacity of existing veterinary professionals, whether through telehealth, AI-assisted diagnostics, or workflow automation, speaks to a quantifiable market need.

Hot: Pet Services Roll-Ups

Dog daycare, boarding, grooming, and training businesses generate recurring revenue from high-frequency, local transactions. They're fragmented across thousands of independent operators. PE loves this setup.

The math is straightforward. A single dog daycare generating $800K in revenue and $150K in EBITDA might trade at 4-5x as a standalone business. Roll fifty of them together, layer in centralized operations and technology, and the multiple expands to 8-12x or higher. Investors bet on the spread.

Cooling: General Pet Food

Pet food businesses that raised during the 2020-2022 funding environment face a harder landscape. Many PE-backed pet food assets are approaching the end of typical 5-7 year holding periods with exit environments less accommodating than their entry conditions suggested.

The challenge is structural. Pet food is a manufacturing business with commodity exposure, thin margins, and retailer power dynamics that limit pricing flexibility. The founders who raised at 2021 valuations now face down-rounds or extended holding periods. New pet food startups struggle to raise because investors watched the last cohort struggle.

Struggling: Hardware Without Software Margins

Pet wearables learned this lesson the hard way. The hardware is commoditizing. GPS chips, accelerometers, and Bluetooth modules get cheaper every year. Differentiation has shifted to software and services, but most wearable companies still price like hardware businesses and margin like hardware businesses.

Investors now ask the software question immediately. What's the recurring revenue? What's the gross margin on the subscription component? If the answer involves selling devices at thin margins and hoping customers upgrade, the meeting ends early.

How Pet Deals Actually Happen

The mechanics of pet industry fundraising differ from what most founder advice assumes. The playbooks written for Bay Area SaaS startups don't map cleanly onto pet.

The Warm Intro Reality

Cold outreach to pet investors has a lower success rate than in most categories. The industry is small enough that investors expect to hear about promising companies through their networks before founders reach out directly. A cold email suggests either the company isn't on anyone's radar or the founder doesn't understand how the industry works.

The implication: founders should work backwards from their target investors. Who in your network knows them? Which portfolio companies could make introductions? What industry events do they attend? The relationship-building often needs to start twelve months before you need the capital.

Events That Matter

SuperZoo (Las Vegas), Global Pet Expo (Orlando), and Pets Plus (UK) concentrate the industry's decision-makers in physical spaces where informal conversations happen. Investors attend not to see booths but to meet founders, hear about deals, and gauge market sentiment.

The founders who get the most value from these events arrive with specific meeting targets and leave with specific next steps. The founders who wander hoping to bump into investors leave with business cards that go nowhere.

Accelerators play a role too. Leap Venture Studio has run ten cohorts of pet startups, with TAW Ventures joining as a strategic partner for Cohort 10. Alumni often cite the network effects as more valuable than the curriculum.

What Gets You a Meeting vs. What Closes a Deal

Getting a meeting requires a credible company with a clear story targeting the right investor at the right stage. This is table stakes. Thousands of pet companies clear this bar annually.

Closing a deal requires something harder to manufacture: conviction that this specific team will win this specific market. Investors pattern-match against their own portfolio successes and failures. They triangulate your claims against their industry sources. They look for reasons to say no, because saying no is easy and saying yes means years of board meetings.

The founders who close understand this asymmetry. They prepare for diligence before it starts. They anticipate objections and address them proactively. They make the investor's job easier by providing clear materials, responsive communication, and reference customers who will pick up the phone.

The Exit Landscape

Who's buying pet companies, at what prices, and on what terms tells you what investors are underwriting when they fund new companies.

Strategic Acquirers Have Specific Criteria

Corporate strategic buyers acquire capabilities they can't build. Zoetis buying Basepaws wasn't about cat DNA tests. It was about the underlying technology and data assets. Mars acquiring Nom Nom wasn't about meal toppers. It was about DTC capabilities and customer relationships.

For founders, this means the strategic exit story requires a clear capability gap narrative. What can you do that they can't? Why is it faster to buy you than build it? These questions determine both whether a deal happens and what multiple you command.

PE Exits and the Holding Period Cliff

Private equity typically holds investments for five to seven years. Assets acquired during the 2018-2020 period are hitting exit windows now, and the environment has shifted. Interest rates are higher. Acquisition multiples have compressed in many categories. Some assets that entered at 12x EBITDA face exits at 8-10x.

The firms that bought well will exit well. The firms that paid 2021 prices for 2021 growth stories face harder conversations. This creates opportunity for buyers with capital and patience, and pressure for sellers who need liquidity.

Valuation Benchmarks

Pet sector M&A transactions averaged 14.5x EBITDA from 2022 through mid-2025. That's a premium to many consumer categories, reflecting both the market's growth characteristics and strategic buyer competition.

Volume tells a different story. Pet M&A fell 37.3% year-over-year to 42 transactions through mid-2025. Strategic buyers still account for 69% of deals, but activity has slowed across the board. Investors expect PE deal-making to increase in 2026 as more assets hit exit windows.

For founders, the implication is nuanced. Premium companies still command premium valuations. But the bar for "premium" has risen, and the timeline to exit has lengthened. Building for acquisition without building a sustainable standalone business is riskier than it was three years ago.

What Sophisticated Founders Do Differently

The founders who consistently raise capital in pet share patterns that separate them from the founders who pitch for years without closing.

They start relationships before they need money. The investor who first hears about your company in a pitch deck has less context than the investor who's been watching your progress for eighteen months. Building investor relationships is a continuous activity, not a fundraising sprint.

They match investor type to company stage. Pitching a growth equity firm on a seed-stage company wastes time. Pitching a dedicated pet VC on a rollup strategy misses the thesis. Sophisticated founders map the investor landscape before they start outreach and target precisely.

They understand portfolio dynamics. If an investor already backs a company in your space, they're unlikely to fund a competitor. But they might introduce you to other investors. Founders who research portfolios before meetings show up prepared to have the right conversation.

They demonstrate proof points that matter for their stage. Seed investors want to see product-market fit signals. Series A investors want to see scalable unit economics. Series B investors want to see a path to category leadership. Presenting the wrong proof points for your stage suggests you don't understand what the investor is evaluating.

The founders who struggle often do so for correctable reasons. They pitch too broadly instead of targeting specifically. They ask for capital before they've built the relationships that generate conviction. They treat all investors as interchangeable rather than understanding the specific criteria each evaluates. The capital is available for companies that fit investor criteria. The work is making your company fit.

The pet industry investor landscape rewards founders who do the work to understand it. The capital exists. The infrastructure of dedicated funds, syndicates, accelerators, and industry angels continues to mature. What's missing isn't opportunity. It's founders who approach fundraising as strategy rather than spray-and-pray.

The investors profiled here have specific criteria, specific timelines, and specific return expectations. The founders who raise efficiently map their companies to those criteria before they start outreach. The founders who raise painfully learn through rejection what they could have learned through research.

You can browse the full archive of pet industry analysis and operator guides at The Underbite Insights.

Affiliated Products

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Suspendisse varius enim in eros elementum tristique. Duis cursus, mi quis viverra ornare, eros dolor interdum nulla, ut commodo diam libero vitae erat.